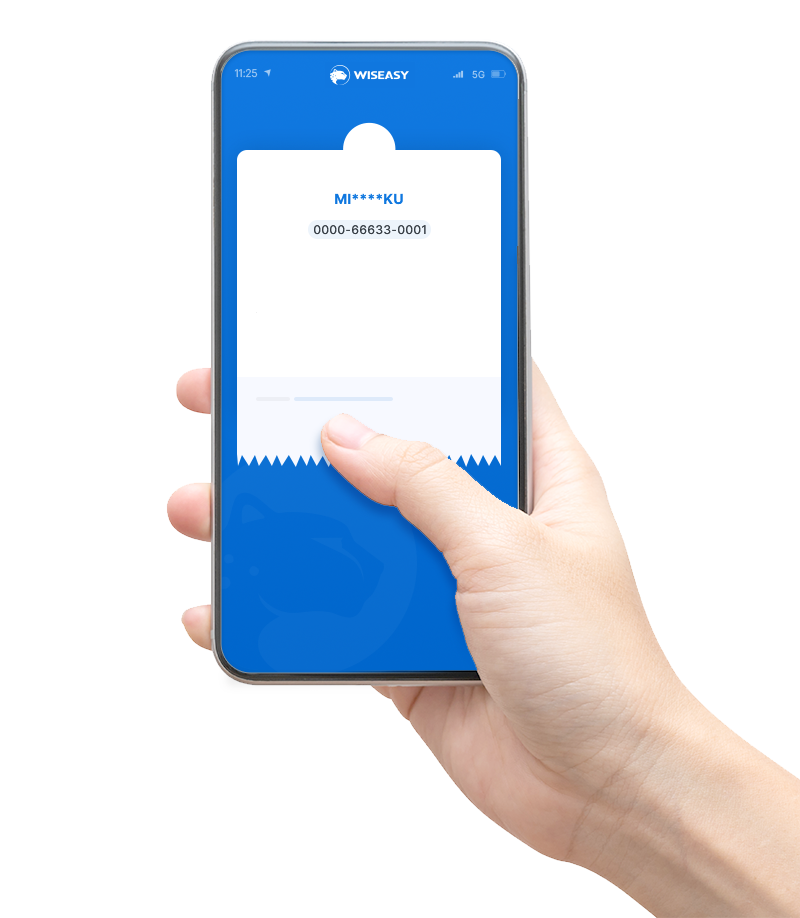

Crafting the Future

of Intelligent Payments, Collaborating Globally.

Our seamless and intelligent payment solutions eliminate friction, unlocking efficiency and precision in every transaction.

Chat With Experts

-¥2000

Rent

-$1,200

Shopping

-$15

coffee

-Rp22.00

Taxi

Amount

2,500,00

Total Amount Sent

$2,500,00